Market Recap FY24: Insights into Indian Equity Markets And Outlook for FY25

Introduction

The FY24 had been a superb year for Indian equity investors. On the back of robust economic growth, Indian markets saw strong interest from domestic as well as international investors. But the year was not smooth sailing all along. We saw some scare in October end, but the market recovered well from the lows. So, in this blog, we will discuss the overall performance of the market and find winners and losers on the sectoral level.

Market Performance

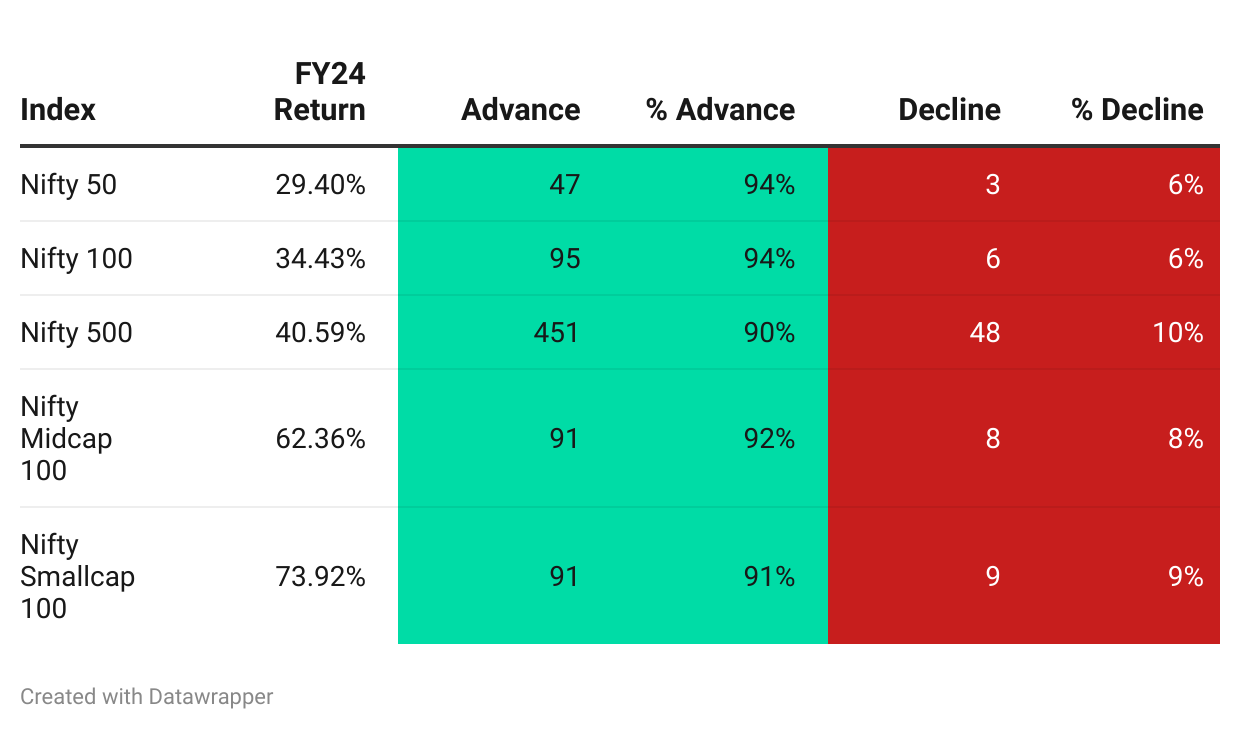

In FY24, the broader market moved with force. The market was in consolidation in CY22. And it moved strongly after the year-long consolidation. All broader indices gave more than 25% returns. But FY24 was the year of mid and small-cap stocks. They were trading at very attractive valuations during the consolidation period of CY22. In FY23, they attracted the investors’ attention due to reasonable valuations and strong business performance.

Nifty Small 100 was the biggest gainer among broader market indices as it generated a whopping 73.92% return in FY24. Those who caught the trend early benefitted immensely in FY24. It was followed by the Nifty Midcap 100 index with an annual return of 62.36%. The advance-decline number shows that this is a broad-based rally. More than 90% of the stocks generated positive returns in FY24.

Large-cap stocks also performed well as Nifty 50 generated a solid 29.40% return in the financial year. But as the size of the company is huge, they have not moved at the same pace.

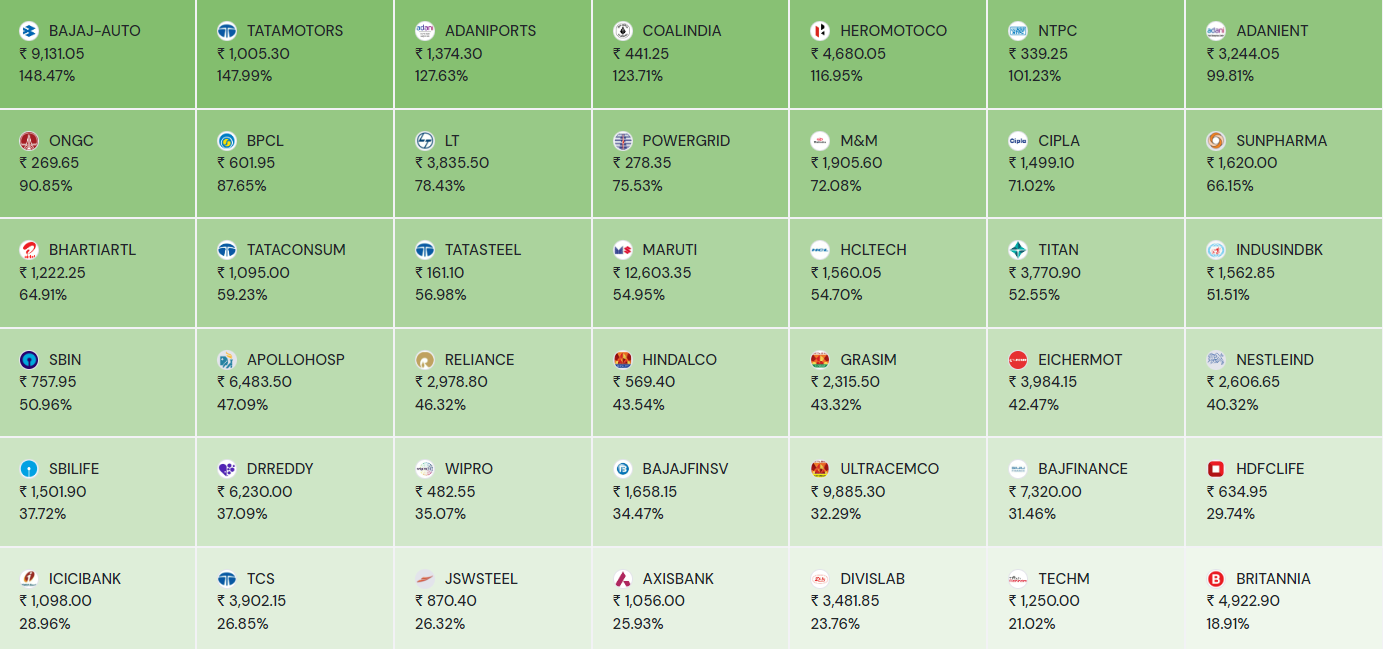

In terms of stocks, many became multi-baggers in FY 24. Six large caps generated more than 100% return in FY 24. You can see the winners from the Nifty 50 universe in the below heatmap.

If we talk about mid and small-cap stocks, 24 stocks from the Nifty Midcap 100 index generated more than 100% return. Top gainers include names like IRFC, REC, RVNL, BHEL, etc. Seven of these names have generated more than 200% returns. You can see the same in the heatmap below.

In Nifty Small-cap 100 stocks, seven names generated more than 300% return and 27 names generated more than 100% return in FY24. Many stocks from this space saw strong momentum and generated superb returns for the investors. As many of the names saw rerating along with strong earnings growth, the price moved at an accelerated pace. You can see the top gainers from Nifty Smallcap 100 stocks in the heatmap below.

So, FY24 was a monstrous year for mid and small-cap stocks as they outperformed the large-cap peers by a huge margin. But will this trend continue in FY25, we have discussed this later in the article.

Sectoral Performance

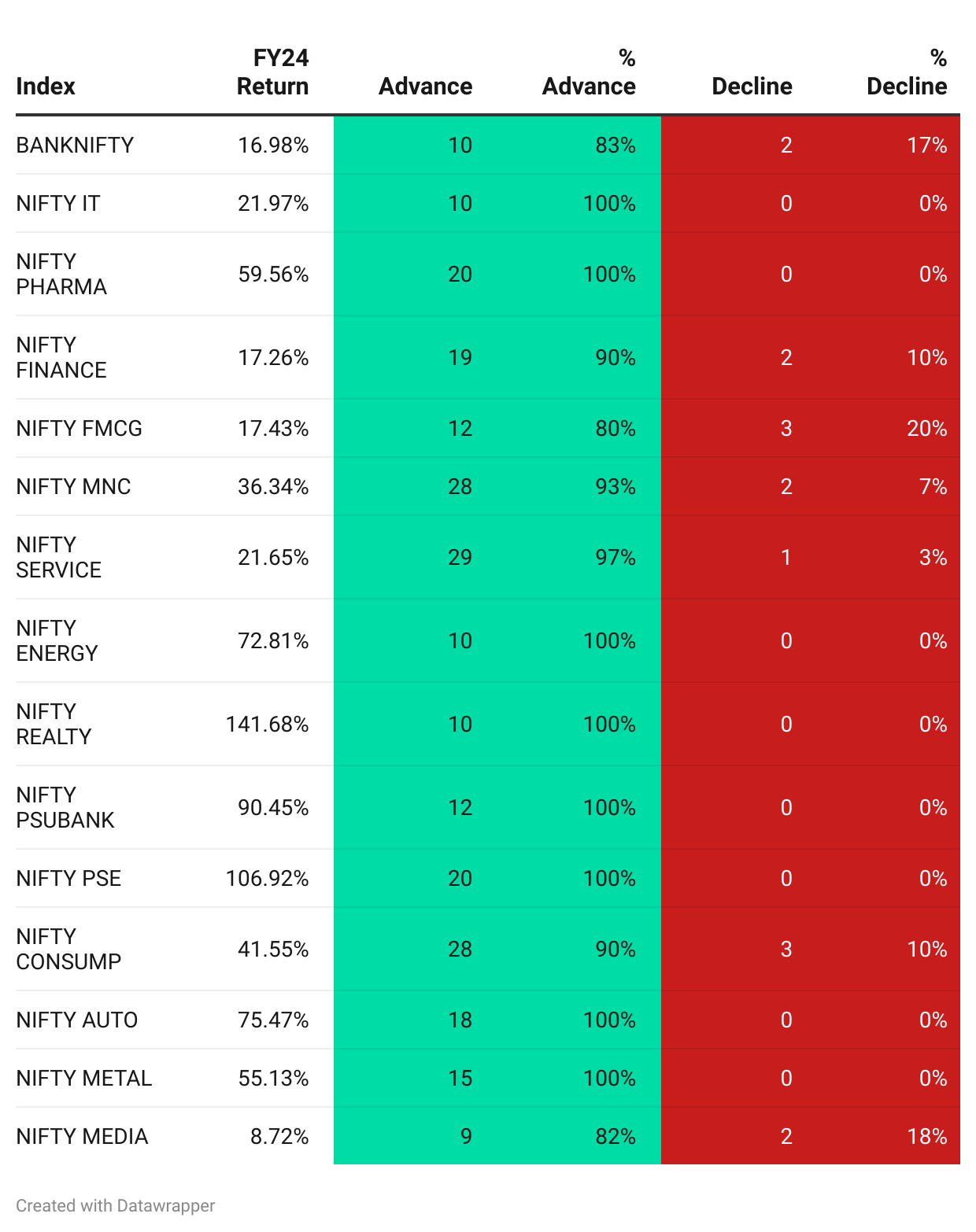

Now let’s focus on sectors. On the sectoral front, apart from the Media sector, all sectors gave double-digit positive returns. PSU companies were the steroids as investors chased them. Initial cheap valuation and strong new orders resulted in the rally and many stocks moved in a straight line. Before sanity returned to the market, many of the PSU names reached euphoric levels.

Apart from PSU companies, realty stocks made a comeback in FY24. Strong pre-sales numbers indicated that the real estate cycle is turning. This sector was in consolidation after the post-COVID rally from October 2021 to June 2023. But after that, it fired on all the cylinders and generated a massive 141.68% return in FY24. It was the top-performing sector of FY24.

Nifty PSE and Nifty PSU Bank secured the second and third place in the list of top-performing sectors. They moved by 106.93% and 90.45% respectively. PSU banks underwent rerating due to their extremely cheap valuation compared to their private peers and improving balance sheet. The interesting thing about PSU banks is that they are still available at a comfortable valuation.

Now let’s look at the top-performing stocks from these sectors. PNB was the top performing company in Bank nifty universe with a return of 169.21%. Interestingly market darling HDFC bank was the worst performer with an annual return of -8.64%. Sobha topped the charts in realty names with a 258.38% return in FY 24. REC and IOB were the top gainers in the PSE and PSU bank space with 298.92% and 188.42% returns respectively. Energy stocks also saw solid traction. IOCL was the top performer among them as it moved up by 117.27% return.

What should we expect in FY 2024-2025?

As the FY24 comes to an end, the question is what should we expect in 2025? Will it be the same as 2024? Well, we feel that we should temper our expectations. As we analyzed in this newsletter, almost all sectors gave more than 20% return. This kind of move does not happen year after year.

As an economy, we have been really strong and we will continue to remain strong. So, we are in a structural bull market. But as we are going to have the general election in the Q1FY25 in seven phases, we may see increased volatility in the market. The current government will likely win, so we do not expect any major policy changes in the coming year.

The central banks around the world (including the RBI) are planning to reduce interest rates in the next six to eight months. So, we may see more liquidity coming into emerging markets like India and that will help the equity market. But most of the pockets in the market are fairly valued or overvalued at the moment. We saw rerating in multiple sectors including PSU and defence. So, companies will show strong earnings growth in the next 12 months, but we feel that this growth is already priced in and the price won’t move at the same pace. So, we should temper our expectations moving forward.

The sectors to watch out for in FY are IT and Chemical. Many IT companies will see large deals won over the last year generating revenue in FY25. Even though the chemical sector is still facing headwinds, the price may stabilize in the first half of FY25 and there can be some recovery in the second half. Some chemical companies have done solid capex and sitting on operating leverage. Once the business momentum comes in, these names will show non-linear earnings growth.

Our two cents of advice will be to stay away from hot sectors. In every upmove in the market, new sectors emerge as winners. So, if you have missed the rally in some of the overheated spaces, don’t try to jump in late. There are enough pockets in the market where you can find strong businesses at the right valuation.

Conclusion

In summary, FY24 was a remarkable year for Indian equities, driven by strong economic growth and market performance. Despite occasional volatility, particularly in late October, the market displayed resilience, with mid and small-cap stocks shining brightest.

Looking forward to FY25, tempered expectations are warranted given the potential for increased volatility surrounding the general election in Q1FY25 and the already elevated valuations in many sectors. While sectors like IT and Chemicals offer promise, investors should exercise caution and focus on fundamentally sound businesses at reasonable valuations.

In essence, while the outlook for FY25 remains positive, a prudent and balanced approach to investing is advisable, prioritizing long-term value creation over short-term gains in overheated sectors.