Position sizing

This parameter is used only in dynamic stock strategy created using the screener or factor model.

Now first things first.

What is position sizing?

Once we have decided which stocks to buy, we need to decide how much of our capital to deploy to each stock. Since we deal with long-only and unleveraged strategies, this essentially boils down to how much of each stock to buy.

And since all strategies are fully deployed, position sizing simplifies deciding the weights of each instrument in our portfolio.

We support 2 weight methods as of now.

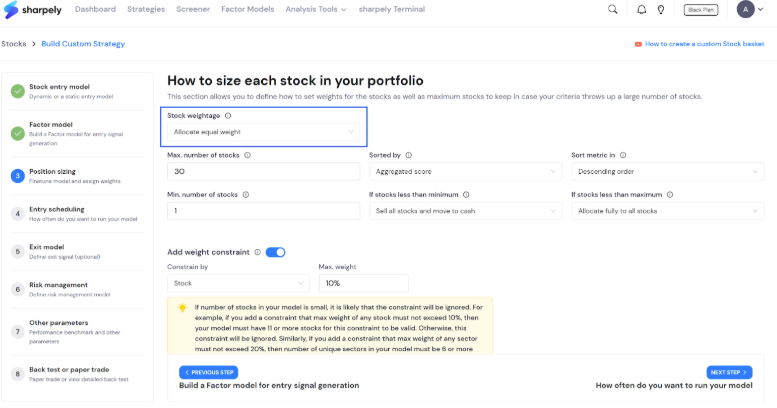

1. Equal weight

This is the simplest method where each stock is weighted equally. So, if you have 10 stocks, each stock will have 10% weight.

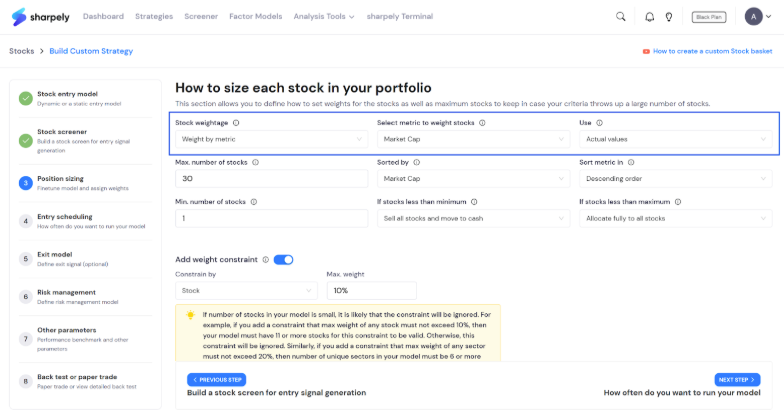

2. Weight by metric

In this case, you can choose to weigh stocks in proportion to a particular metric's value. The most used metric in this case is the market capitalization of the stock.

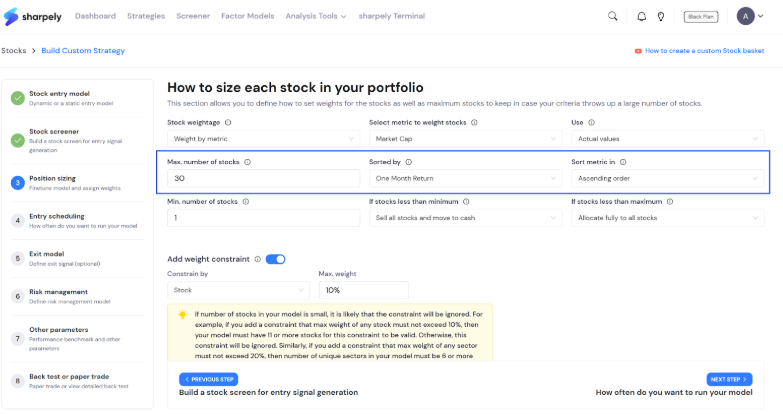

But just deciding how we allocate the funds is not enough. We have to decide how many stocks you want to invest in. For example, you have created a screener and 65 stocks get screened. Now, you won’t be investing in all 65 of them. You will limit the number to maybe 20 or 30.

Deciding the maximum number of stocks

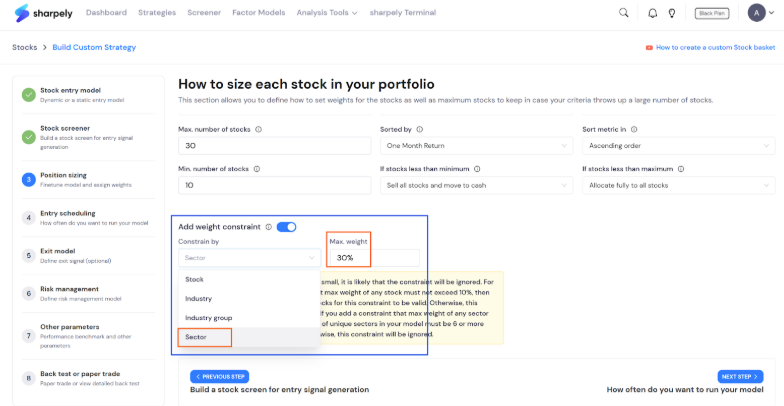

Here you can define how many stocks you want to include in your portfolio and based on what metric. Let’s continue with our example. Out of 65 stocks, we want to invest in the top 30 stocks that have given the highest one-month return. You can do this very easily as shown in the image below.

Here you can choose any metric. You can select 30 stocks with the lowest PE or highest ROE or any metric of your choice.

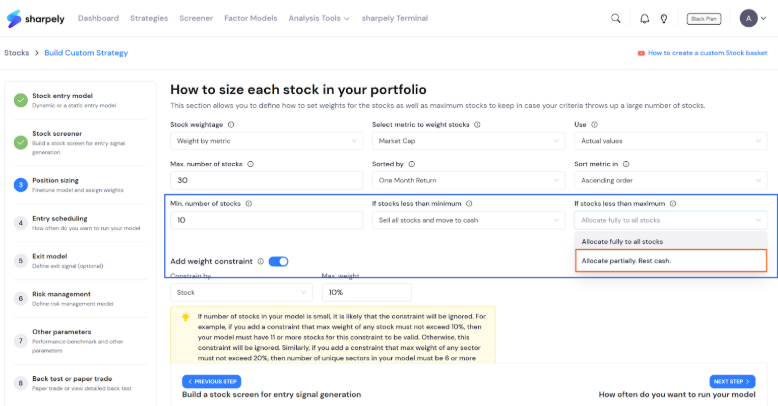

Define the minimum number of stocks

But just defining the maximum number of stocks is not enough. You should also decide what to do when the screened stocks fall below the maximum limit. For example, if a market downturn comes and you have only 10 screened stocks. Then will you allocate all the funds in this stock equally or you will partially allocate the funds and the rest of the funds will remain in cash?

On sharpely, you can customize that as well. Read the next lines very carefully (maybe read them again if you need to). Let’s say you have decided that the minimum number of stocks in your portfolio is 10. If the number falls below 10 you will sell everything and stay in cash. But if the number is between 10(minimum) and 30(maximum), then you will allocate partially in the rest will be held in cash. And this is how you can do that on sharpely

So if you have invested Rs. 300000 in 30 stocks equally and the number of stocks falls to 20. Only Rs. 200000 will be deployed and the rest will be held in cash.

Reducing concentration risk

The last but not the least, you should also reduce the concentration risk. In simple terms, you should avoid investing very heavily in one stock or sector. Because if that particular stock/sector sees heavy selling, then your whole portfolio will suffer.

Guess what? sharpely allows limit that exposure as well! Let’s say you want to limit the sector exposure to 30%. You can do that easily as shown in the below image!

And that is how you define the position sizing. To summarize, there are four main parts. Define how you will allocate funds, the maximum number of stocks, the minimum number of stocks and exposure.

In the next article, we will look at the ‘ Entry Scheduling ’.